What Is Capital Gains Tax? 2026 Rates Explained

As tax season wraps up, many investors may be reviewing what drove their tax bill last year. For many, capital gains taxes could have played a significant role.

If your tax professional didn’t walk you through how capital gains tax works or proactively look for ways to offset it for you, it might be time to explore other options. Capital gains tax is a vital part of tax planning that should be considered throughout the year, not only as you scramble to submit your return on time. Understanding the rules that drive this tax today may help you plan more intentionally for the future.

2026 Capital Gains Tax: Key Takeaways

- Capital gains tax is owed when you sell an asset for more than its adjusted cost basis.

- Short-term capital gains (assets held one year or less) are taxed at ordinary income tax rates.

- Long-term capital gains (assets held more than one year) are taxed at 0%, 15%, or 20%, depending on taxable income and filing status.

- 2026 capital gains tax brackets vary by filing status and taxable income.

What is Capital Gains Tax?

Capital gains tax is the tax owed on the profit from selling an asset for more than your adjusted cost basis (generally what you paid for it, plus certain adjustments).

Of course, it’s a welcome thing to profit from selling your capital assets. That’s a good problem to have! However, when you do so, it’s important to plan for the increased tax bill.

Capital gains tax is most often associated with assets such as:

- Investments (stocks, bonds, mutual funds, ETFs)

- Real estate

- Personal property (car, home, furniture)

- Business holdings

It’s important to note that mutual funds distribute capital gains at the end of each year, which may create taxable income even if you didn’t personally sell shares.

Capital gains are typically realized when you:

- Sell appreciated investments

- Receive capital gain distributions from funds

- Exit a business or real estate holding

- Rebalance or unwind concentrated positions

How much capital gains tax you owe depends primarily on two factors:

- How long you held the asset

- Your taxable income and filing status in the year of sale

Realized vs. Unrealized vs. Recognized Gains

Realized gain is the profit made when an asset is sold or transferred. Unrealized gain is the increase in the value of a capital asset that you have not yet sold, or the “on paper profit”. Recognized gain is the portion of the realized gain that is taxable and must be reported on your tax return.

Not every realized capital gain or loss is fully recognized in the current tax year. This can occur in certain exchanges, exclusions, deferrals, or tax-advantaged accounts. For example, gains and losses held in tax-advantaged accounts such as IRAs, 401ks, HSAs, and 529s are generally not taxable in the year realized. Losses on personal-use property are unfortunately never tax-deductible. However, in certain situations, capital gains tax can be postponed until future tax years.

It is especially essential for business owners, real estate investors, and those using proactive tax planning strategies to understand these distinctions.

Short-term Capital Gains Tax

A short-term capital gain occurs when you sell an asset held for one year or less at a profit. These gains are taxed at ordinary income tax rates. Your ordinary income tax rate is the rate that applies to your wages and non-qualified income. These rates are typically higher, so it’s usually not tax-efficient to sell at a profit within a year of purchase.

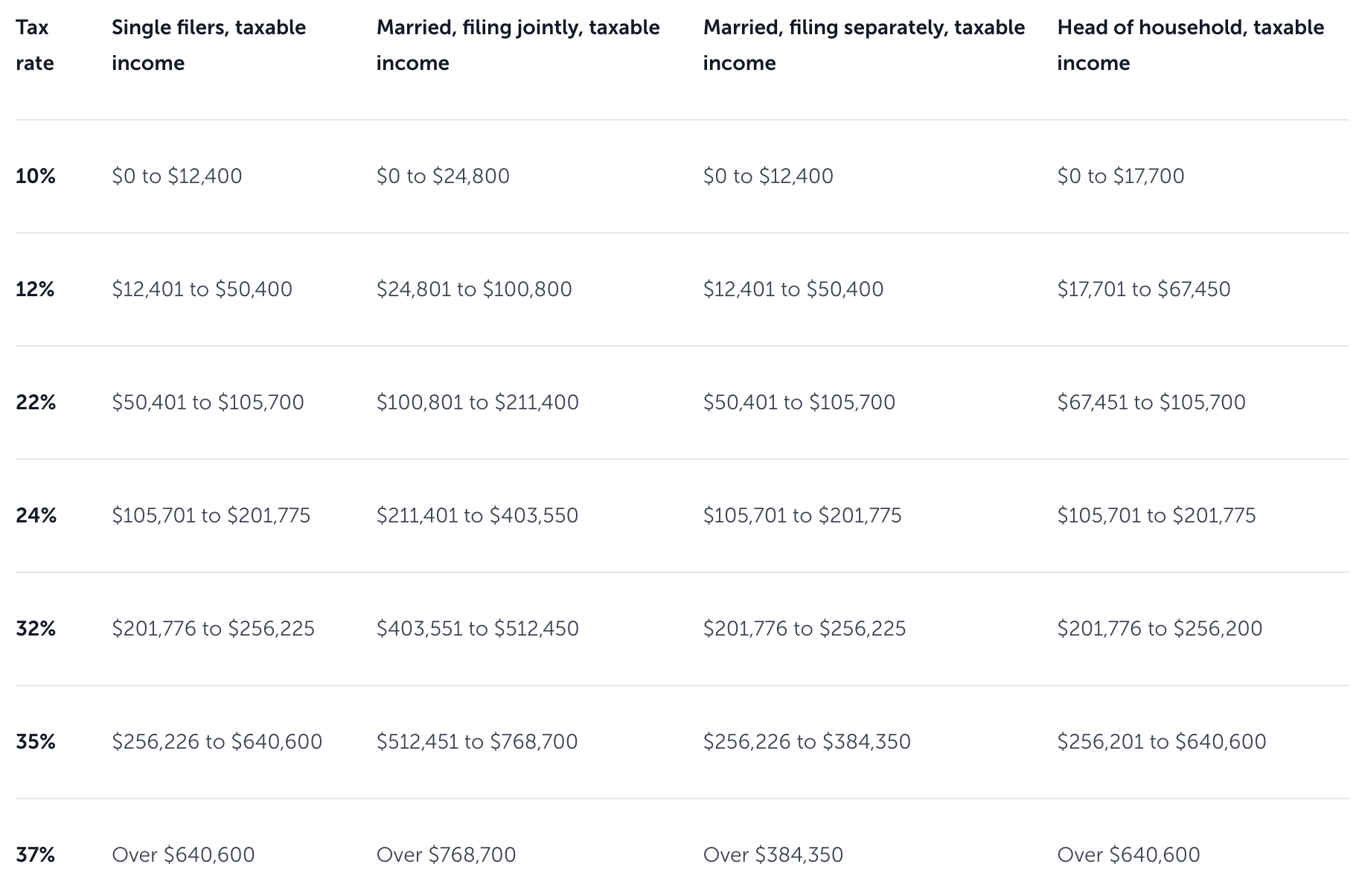

2026 Short-term Capital Gains Tax Brackets

Short-term capital gains are taxed according to the 2026 ordinary income tax brackets. These are progressive and graduated rates, meaning income is taxed in layers. Your exact short-term capital gains tax rate depends on your total taxable income and filing status.

For 2026, federal ordinary income tax rates are:

Long-term Capital Gains Tax

A long-term capital gain occurs when you sell an asset held for one year and one day or more at a profit. These are taxed at preferential rates (0%, 15%, or 20%) when realized and recognized. Your threshold is based on your taxable income, including the capital gain, and filing status. Since these rates are typically lower, one of the simplest ways to reduce capital gains tax is to hold assets for over a year.

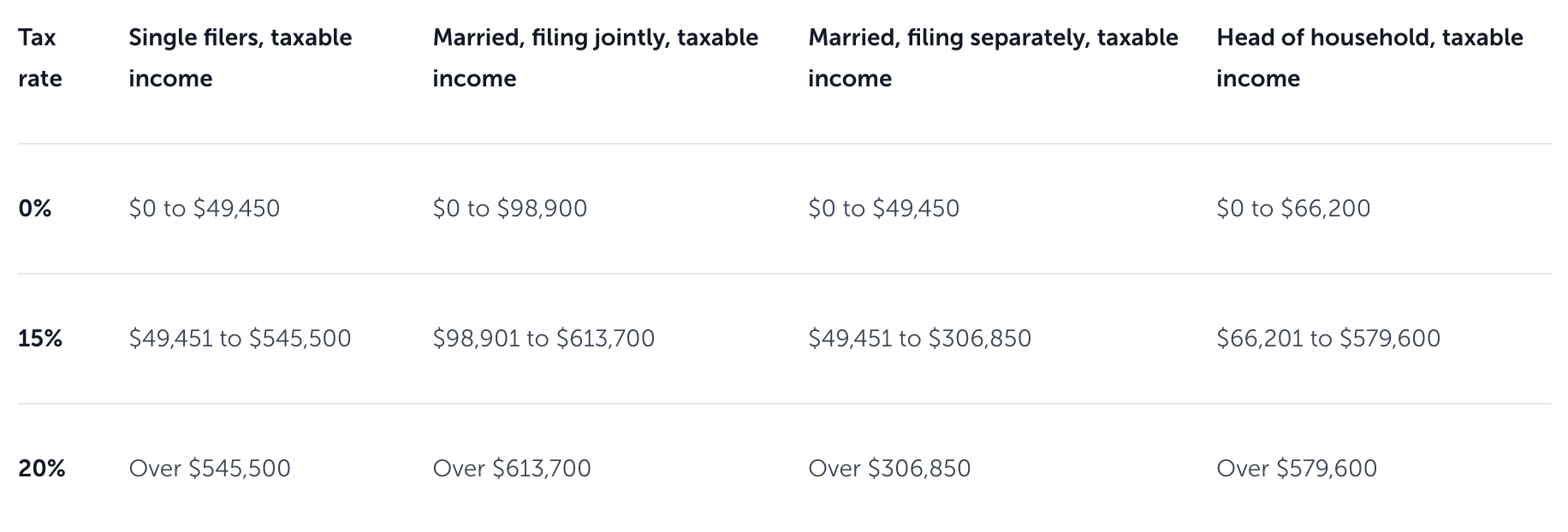

2026 Long-term Capital Gains Tax Brackets

Long-term capital gains tax brackets are separate from ordinary income tax brackets. While thresholds may change due to legislation, the structure has historically remained consistent.

For 2026, federal capital gains tax rates are:

Higher-income households may also need to account for the Net Investment Income Tax (NIIT). NIIT is an additional 3.8% surtax that applies once income exceeds certain levels.

Final Thoughts on Capital Gains Taxes

Capital gains tax is an expected side effect of successful investing. The key to minimization is understanding when gains are realized, how they are taxed, and which bracket applies to your situation.

A proactive approach throughout can make a substantial difference in your after-tax results. If capital gains caught you and your tax bill off guard this year, we’d love to help coordinate your future approach. If you anticipate a large sale, liquidity event, or portfolio transition in the future, let us help you coordinate those decisions with a broader investment and wealth management strategy.

FAQs About Capital Gains Taxes

What is the tax rate on capital gains?

The capital gains tax rate depends on how long the asset was held, your taxable income, and your filing status in the year of sale. Short-term capital gains are taxed at ordinary income tax rates (federally 10% to 37%). Long-term capital gains are taxed at 0%, 15%, or 20%, based on taxable income and filing status, plus a potential 3.8% Net Investment Income Tax for high-income households.

How do I avoid capital gains on my taxes?

Capital gains generally cannot be avoided entirely when an asset is sold at a profit. However, strategies such as holding assets for more than one year, coordinating income timing, and thoughtful planning may reduce the overall tax impact. A proactive investment and tax strategy is often the most effective approach.

Thinking about how this applies to you?

If this topic connects to decisions you’re facing, Beacon Hill Private Wealth helps clients evaluate planning, investment, and tax considerations in context and over time.

Request an introductory conversation

Beacon Hill Private Wealth is an independent, fee-only fiduciary investment advisory firm. Founder Tom Geoghegan provides coordinated wealth management that integrates evidence-based investing with tax-aware financial planning, helping professionals and families navigate complex financial decisions over time.

For informational purposes only. The content does not purport to present a complete picture, but Focus Partners believes the information is representative of issues and needs facing some clients. This should not be construed as specific investment, tax, or legal advice. Individuals should seek advice from their wealth advisor or other advisors before undertaking actions in response to the matters discussed. No client or prospective should assume the above information serves as the receipt of, or substitute for, personalized individual advice. This reflects the opinions of Focus Partners or its representatives, may contain forward-looking statements, and presents information that may change. Nothing contained in this communication may be relied upon as a guarantee, promise, assurance, or representation as to the future. Past performance does not guarantee future results. Market conditions can vary widely over time, and certain market and economic events having a positive impact on performance may not repeat themselves. Investing involves risk, including, but not limited to, loss of principal. The appropriateness of a particular investment or strategy will depend on an investor's individual circumstances and objectives. This is prepared using third-party sources considered to be reliable; however, accuracy or completeness cannot be guaranteed. The information provided will not be updated any time after the date of publication. ©2026 Focus Partners Wealth, LLC. All rights reserved. RO-26-5237101