Save More on Taxes: Planning Strategies to Review Before Year-End

Contrary to popular belief, taxes aren’t just a chore for the early spring. Rather, tax planning and preparation is a four-season affair.

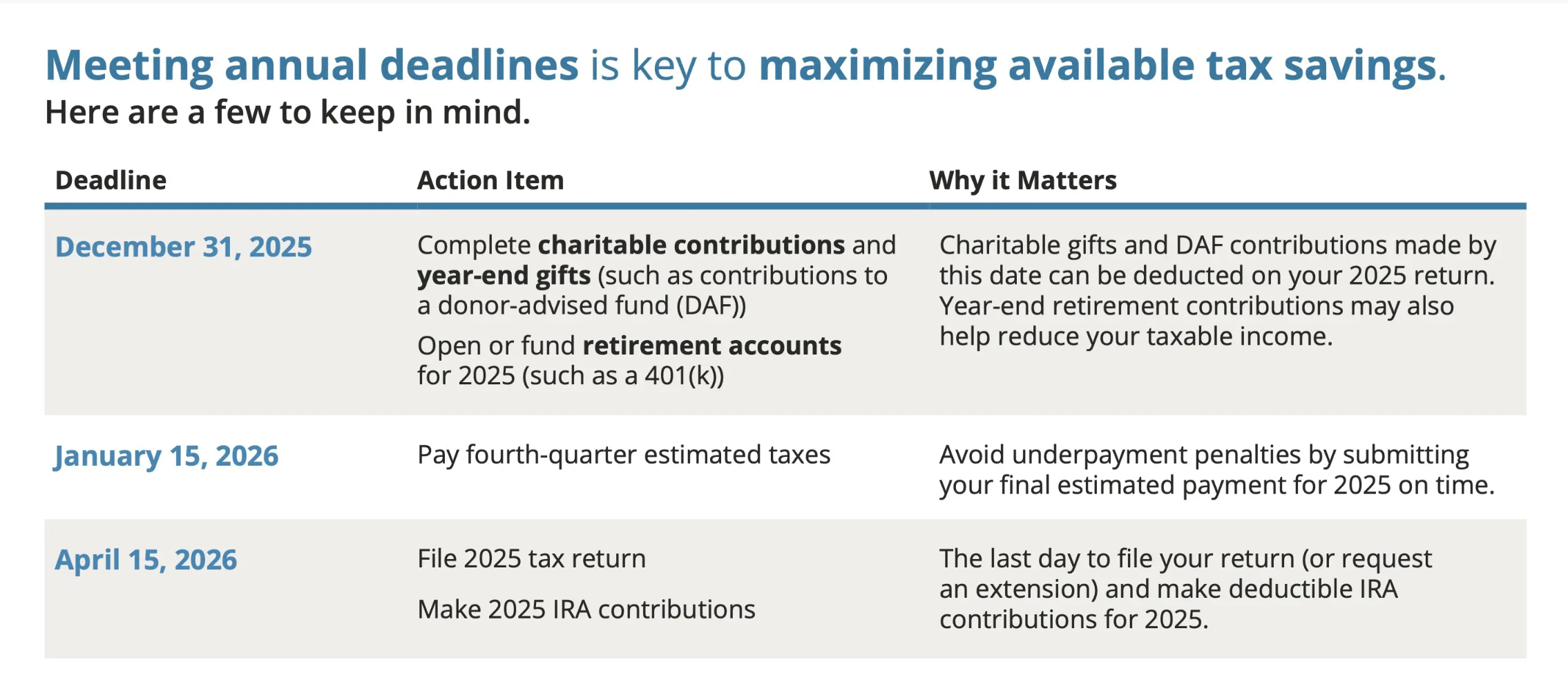

In fact, some of the most impactful tax planning should be implemented ahead of the year-end deadline. For most taxpayers there is little wiggle room after December 31. Here are some common tax planning strategies to consider before year-end.

Maximizing Deductions

Taxpayers have the option of opting into the flat standard deduction or choosing to itemize deductions. Itemizing requires better record-keeping and usually a professional tax preparer but can result in significant tax savings for the taxpayer.

Some taxpayers reside in a gray area where they have slightly too few deductions to make itemizing worthwhile. This is where “bunching” comes into play. Taxpayers can bunch or cluster these deductions around a single year, making itemizing a no-brainer every few years. Common deductions like property taxes, planned medical expenses, and even mortgage interest expenses can be strategically timed for maximum tax savings.

Charitable Giving

There are three common charitable giving strategies that should be executed before year-end so tax savings can be included on a taxpayer’s return.

- Donating appreciated securities allows donors to get credit for the current market value, while not realizing taxes on the gain. This serves to both maximize giving and reduce tax exposure for the donor. (Note: Donated securities are limited to 30% of adjusted gross income (AGI), while excess donations may be carried forward up to five years).

- Many retirees are subject to mandatory distributions from a traditional IRA known as required minimum distributions (RMDs), which are taxable. Taxpayers can characterize these distributions as qualified charitable contributions (QCDs) and send them directly from their IRA to a charity. QCDs are nontaxable and satisfy the RMD requirements for the taxpayer.

- Lastly, some taxpayers may want to take advantage of bunching or deduction clustering in order to itemize their deductions. If this is the case, contributing to a donor-advised fund (DAF) may be helpful. DAFs allow for a large one-time contribution (and tax deduction), which is then distributed to the charities over the following years.

Maxing Out Retirement Accounts

Tax-advantaged retirement accounts are one of the best tools available to investors. Employees should seek to maximize these tax-advantaged accounts either to defer income from peak earning years or to lock in taxes at lower income levels.

The deadline for annual contributions is December 31 for company plans like 401(k)s, 403(b)s, and SEP IRAs. Other IRA accounts like traditional or Roth IRAs have an April 15 contribution deadline for the following year, giving earners a little over five quarters to earn and contribute income.

Review “Other” Compensation Opportunities

As the end of the year draws near, it is worth reviewing compensation outside of salary for year-end tax planning opportunities. Vesting across equity compensation plans—such as employee stock ownership plans (ESOPS) and restricted stock units (RSUs)—may provide valuable tax planning opportunities.

Employees should review their contributions to flexible spending accounts (FSAs) and health saving accounts (HSAs) for the year. FSAs are “use it or lose it” accounts, meaning that any balance remaining at the end of the year may be forfeited after a short grace period. This balance should inform contribution amounts for the following year, too. Dependent care FSAs and deferred compensation opportunities are other often overlooked areas to minimize lifetime tax rates.

Investing in Education

While 529 plans have high contribution limits, gift taxes may apply when gifting more than the annual exclusion amount. If you’re looking to contribute to a child’s education, be sure to fund these accounts prior to year-end.

College-aged adults have until the year’s end to generate enough income to take advantage of various education-related tax credits. These college students may have generous parents willing to match earnings in Roth IRAs as well. Although the earned income deadline is December 31 of the prior year, Roth IRA contributions can be made until April 15 of the following year.

Income Timing

Real estate and passive income may offer some ability to be timed or delayed. Real estate expenses can be delayed or accelerated to maximize the deduction available to the professional. These opportunities to “bunch” deductions around certain years are valuable. Taxpayers can plan to opt into itemized deductions, potentially reducing their tax bill substantially.

It may make sense for certain families to gift income-producing assets to children or family members in lower tax brackets. This removes significantly appreciating assets from their estate while providing for tax savings by shifting assets to those in lower marginal brackets.

Capital Gains

Significant capital gains can leave taxpayers with a surprise tax bill. Leveraged long-short strategies funded today can mitigate this tax bill somewhat this year and reduce it in the future.

Qualified opportunity zone investments may offer unique tax benefits this year by deferring gains into the future and potentially eliminating taxes on future growth.

Small Business Planning

Small businesses can take advantage of qualified business income (QBI) deductions for eligible sole proprietors, partnerships, LLCs, and S corporations. QBI is far too valuable of an opportunity to miss out on for these small business owners, so please consult with your financial advisor or tax accountant to make sure you’re taking advantage of QBI, if available.

Plan to Maximize Gifts and Estate Transfers

Annual giving limits put a cap on consequence-free taxes for annual giving, but maximizing these gifts during the year allows for the largest and most tax-efficient intergenerational transfer of wealth. These strategies are especially valuable in the context of large estate planning for high-net-worth families.

Not sure if you’re making the most of available tax strategies before year-end? Let’s talk through your options together.

Thinking about how this applies to you?

If this topic connects to decisions you’re facing, Beacon Hill Private Wealth helps clients evaluate planning, investment, and tax considerations in context and over time.

Request an introductory conversation

Beacon Hill Private Wealth is an independent, fee-only fiduciary investment advisory firm. Founder Tom Geoghegan works with individuals and families nationwide and has shared insights with national outlets including Bloomberg, CNBC, and Barron’s. View selected media mentions.

This communication is for informational purposes only. The content does not purport to present a complete picture, but Beacon Hill believes the information is representative of issues and needs facing some clients. This should not be construed as specific investment, tax, or legal advice. Individuals should seek advice from their wealth advisor or other advisors before undertaking actions in response to the matters discussed. No client or prospective client should assume the above information serves as the receipt of, or substitute for, personalized individual advice. This represents the opinions of Beacon Hill and presents information that may change. Nothing contained in this presentation may be relied upon as a guarantee, promise, assurance, or representation as to the future. Investing involves risk, including, but not limited to, loss of principal. The appropriateness of a particular investment or strategy will depend on an investor’s individual circumstances and objectives. This is prepared using third party sources considered to be reliable; however, accuracy or completeness cannot be guaranteed. The information provided will not be updated any time after the date of publication. ©2025 Focus Partners Advisor Solutions, LLC. All rights reserved. RO-25-4953257