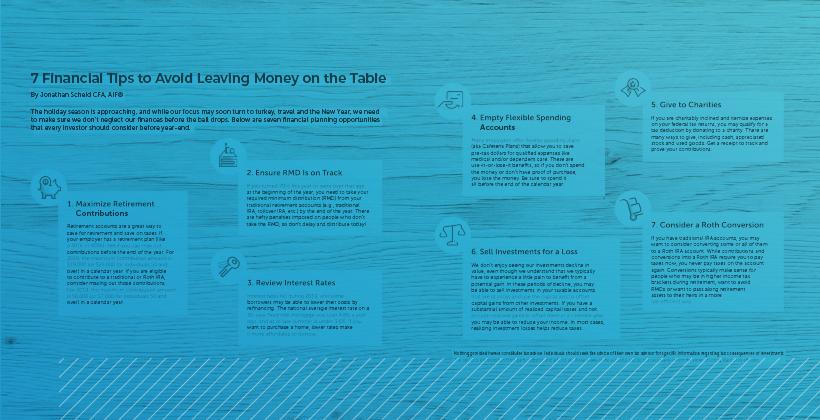

7 Financial Tips to Avoid Leaving Money on the Table

The holiday season is approaching, and while our focus may soon turn to turkey, travel and the New Year, we need to make sure we don’t neglect our finances before the ball drops. Below are seven financial planning opportunities that every investor should consider before year-end.

1. Maximize Retirement Contributions

Retirement accounts are a great way to save for retirement and save on taxes. If your employer has a retirement plan (like a 401k or 403b), see if you can max out contributions before the end of the year. For 2019, the maximum contribution amount is $19,000 (or $25,000 for individuals 50 and over) in a calendar year. If you are eligible to contribute to a traditional or Roth IRA, consider maxing out those contributions. For 2019, the maximum contribution amount is $6,000 (or $7,000 for individuals 50 and over) in a calendar year.

2. Ensure RMD Is on Track

If you turned 70½ this year or were over that age at the beginning of the year, you need to take your required minimum distribution (RMD) from your traditional retirement accounts (e.g., traditional IRA, rollover IRA, etc.) by the end of the year. There are hefty penalties imposed on people who don’t take the RMD, so don’t delay and distribute today.

3. Review Interest Rates

Interest rates fell during 2019, and some borrowers may be able to lower their costs by refinancing. The national average interest rate on a 30-year fixed-rate mortgage was over 4.8% a year ago, and as of late summer is under 3.6%. If you want to purchase a home, lower rates make it more affordable to borrow.

4. Empty Flexible Spending Accounts

Many employers offer flexible spending plans (aka Cafeteria Plans) that allow you to save pre-tax dollars for qualified expenses like medical and/or dependent care. These are use-it-or-lose-it benefits, so if you don’t spend the money or don’t have proof of purchase, you lose the money. Be sure to spend it all before the end of the calendar year.

5. Give to Charities

If you are charitably inclined and itemize expenses on your federal tax returns, you may qualify for a tax deduction by donating to a charity. There are many ways to give, including cash, appreciated stock and used goods. Get a receipt to track and prove your contributions.

6. Sell Investments for a Loss

We don’t enjoy seeing our investments decline in value, even though we understand that we typically have to experience a little pain to benefit from a potential gain. In these periods of decline, you may be able to sell investments in your taxable accounts that are at a loss and use the capital loss to offset capital gains from other investments. If you have a substantial amount of realized capital losses and not enough realized gains to offset them in a calendar year, you may be able to reduce your income. In most cases, realizing investment losses helps reduce taxes.

7. Consider a Roth Conversion

If you have traditional IRA accounts, you may want to consider converting some or all of them to a Roth IRA account. While contributions and conversions into a Roth IRA require you to pay taxes now, you never pay taxes on the account again. Conversions typically make sense for people who may be in higher income tax brackets during retirement, want to avoid RMDs or want to pass along retirement assets to their heirs in a more tax-efficient way.

Jonathan Scheid is the Vice President of Portfolio Strategy & Education for Loring Ward

Nothing provided herein constitutes tax advice. Individuals should seek the advice of their own tax advisor for specific information regarding tax consequences of investments.

Beacon Hill Private Wealth is an independent, fee-only, fiduciary investment advisor providing evidence-based wealth planning solutions that simplify our clients' financial lives. Founder Tom Geoghegan, CFP®, MBA is also a member of the National Association of Personal Financial Advisors (NAPFA).

This material and any opinions contained are derived from sources believed to be reliable, but its accuracy and the opinions based thereon are not guaranteed. The content of this publication is for general information only and is not intended to serve as specific financial, accounting or tax advice. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security. Please consult legal or tax professionals for specific information regarding your individual situation.

By clicking on any of the links above, you acknowledge that they are solely for your convenience, and do not necessarily imply any affiliations, sponsorships, endorsements or representations whatsoever by us regarding third-party Web sites. We are not responsible for the content, availability or privacy policies of these sites, and shall not be responsible or liable for any information, opinions, advice, products or services available on or through them.

Past performance is no guarantee of future results. There is no guarantee investment strategies will be successful. Investing involves risks including possible loss of principal. Investors should talk to their financial advisor prior to making any investment decision. There is always the risk that an investor may lose money. A long-term investment approach cannot guarantee a profit.