Managing Dividend Income to Improve Your Tax Health

When it comes to taxes, not all dividend income is the same. Qualified and nonqualified dividends have different implications for your portfolio’s tax efficiency, just as HDL and LDL cholesterol have different implications for your health.

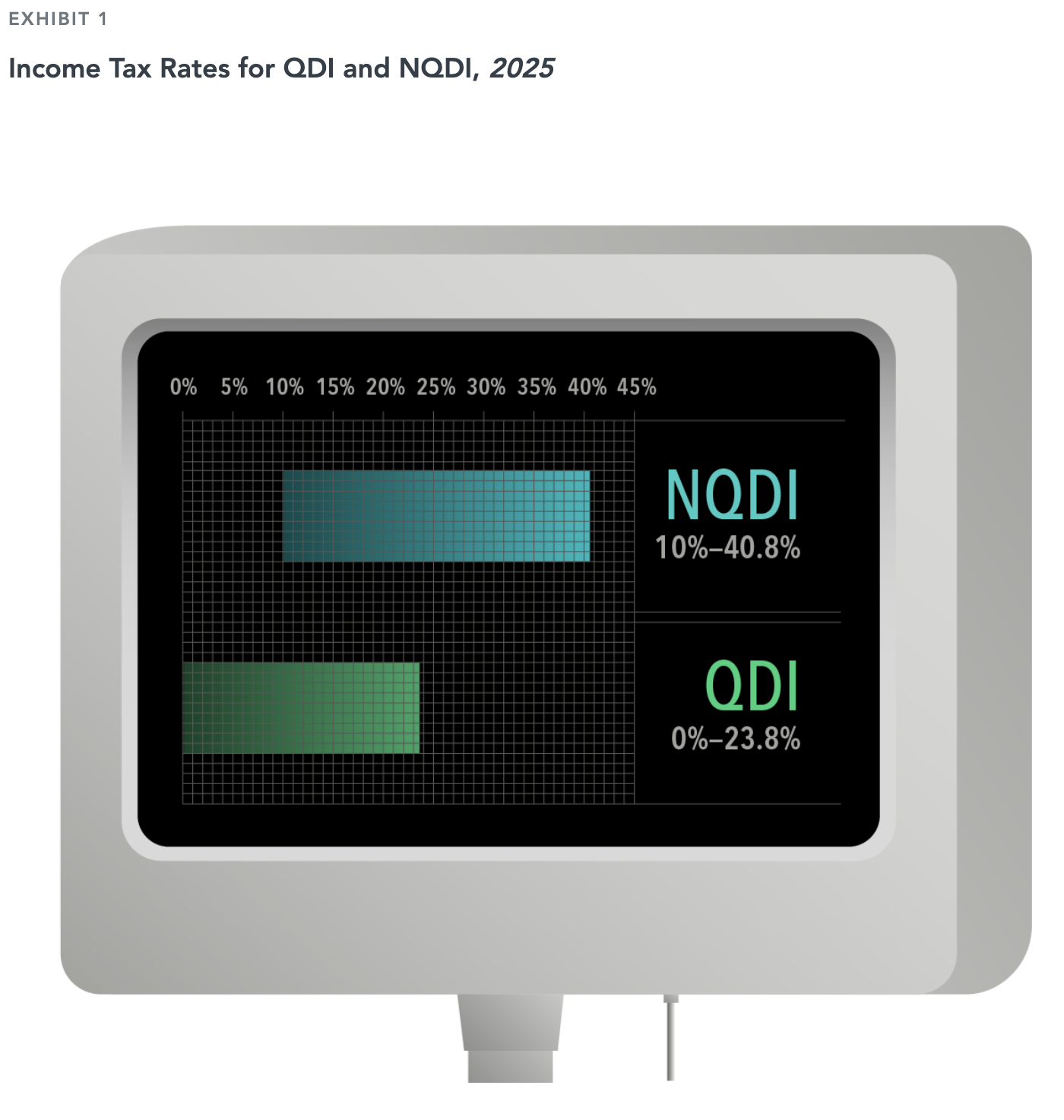

Qualified income, or QDI, is generally taxed at lower rates in the United States than nonqualified income (NQDI). In 2025, the maximum tax rate for NQDI was 40.8%, compared to 23.8% for QDI.1 Like LDL, the “bad kind” of cholesterol, NQDI requires strategies to keep it in check. For a portfolio manager, increasing the percentage of total income that is qualified starts with understanding the sources of income in a portfolio.

NQDI can arise from several sources. One is the type of securities the portfolio may hold. For example, income from real estate investment trusts (REITs) is typically treated as NQDI. Another source is trading activity. Having the flexibility to consider minimum holding periods around dividend payment dates when buying and selling securities can help reduce unnecessary NQDI.

Maximizing the extent to which income is qualified can be beneficial for tax outcomes, just as tracking your cholesterol can help improve health outcomes.

By Karen Umland, CFA Senior Investment Director and Vice President and Ashley Cruz Senior Investment Strategist and Vice President of Dimensional Fund Advisors.

Beacon Hill Private Wealth is an independent, fee-only, fiduciary investment advisor providing evidence-based wealth planning solutions that simplify our clients' financial lives. Founder Tom Geoghegan, CFP®, CIMA®, CPWA®, RMA® is also a member of the National Association of Personal Financial Advisors (NAPFA).

The information provided is educational and general in nature and is not intended to be, nor should it be construed as, specific investment, tax, or legal advice. Individuals should seek advice from their wealth advisor or other advisors before undertaking actions in response to the matters discussed. No client or prospective should assume the above information serves as the receipt of, or substitute for, personalized individual advice.

This reflects the opinions of Beacon Hill Private Wealth or its representatives, may contain forward-looking statements, and presents information that may change. Nothing contained in this communication may be relied upon as a guarantee, promise, assurance, or representation as to the future. Past performance does not guarantee future results. Market conditions can vary widely over time, and certain market and economic events having a positive impact on performance may not repeat themselves. Investing involves risk, including, but not limited to, loss of principal. Asset allocation and diversification may be used in an effort to manage risk and enhance returns. However, no investment strategy or risk management technique can ensure profitable returns or protect against risk in any market environment. Beacon Hill's opinions may change over time due to market conditions and other factors. The appropriateness of a particular investment or strategy will depend on an investor's individual circumstances and objectives.